The US, Israel and Iran War

The conflict continues to dominate global news and financial markets.

In last month’s letter, we outlined a scenario where sustained military pressure could significantly degrade Iran’s offensive capability and potentially encourage regime change, without leading to a large-scale US ground invasion. Failing this, a truce could emerge, likely involving the reopening of the Strait of Hormuz in exchange for the US and Israel winding down their military operations.

Likewise, while the US and Israel may prevail in a short conflict, a prolonged war risks triggering a significant global economic downturn. For this reason, some level of de-escalation remained the most likely outcome.

Now, six weeks into the conflict, a tentative two-week truce may hold. Under this arrangement, US and Israeli airstrikes have paused, while Iran is to allow shipping through the Strait of Hormuz. Markets initially responded positively. However, while this is a step toward normalisation, we remain cautious on the medium-term outlook.

Despite the military imbalance, Iran retains a powerful lever: the ability to threaten shipping through the Strait. Even the risk of disruption provides significant economic leverage. Under pressure from both the US and key trading partners such as China, Iran appears willing to allow passage—but likely at a cost.

Reports suggest Iran may impose a toll on vessels transiting the Strait. Given tanker capacities of 1–2 million barrels, a fee of around $2 million per vessel equates to roughly $1 – $2 per barrel. With historically 90–125 non-Iranian ships passing through daily, this could become a meaningful revenue source for Iran.

It is arguably in Iran’s interest to reopen the Strait gradually, maintaining pressure while maximising future toll revenues. We expect oil and gas flows to resume, but at reduced capacity over the coming months. This follows an effective shutdown over the past six weeks, which has materially drawn down Asian fuel reserves; particularly relevant for Australia.

Revisiting the 1970’s Oil Shock and its impact on the US Share Market

Over the past month, we have revisited the oil shock of the 1970s. While the Yom Kippur War lasted only 20 days, the resulting oil embargo by Arab producers persisted for approximately five months.

Even after supply resumed, oil prices remained elevated. This drove sustained inflation, increased costs for households and businesses, and slowed economic growth. Interest rates rose sharply, and equity markets declined.

Six months after the conflict began, the Dow Jones Industrial Average had fallen around 17% from its 1973 peak. However, the most severe phase of the downturn occurred approximately eight months after the war began. From peak to trough, the Dow declined by roughly 45%.

This period also marked the collapse of the “Nifty Fifty”.

The Nifty Fifty comprised dominant US companies such as Coca-Cola, IBM, Johnson & Johnson and McDonald’s. These were considered “one-decision” stocks — buy, hold indefinitely and disregard valuation.

By the early 1970s, this thinking had driven valuations to extreme levels, with many stocks trading on multiples of 40x, 50x, or higher. The businesses themselves remained strong; the issue was that prices had become disconnected from fundamentals.

As inflation rose and interest rates increased, valuations compressed sharply. Many of these stocks declined by 50% or more, despite their underlying quality. Crowded positioning amplified the downturn as investors exited simultaneously.

Arguably there are some parallels today in the Australian market, where index-driven buying has concentrated capital into larger companies. This has resulted in elevated valuations relative to historical averages. Similarly, US markets remain heavily influenced by large technology companies.

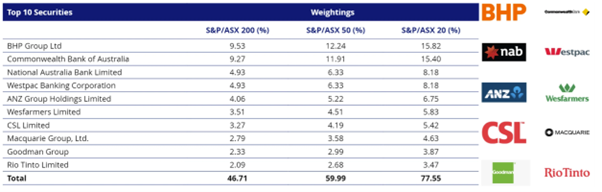

The concentration is evident in the following table, with approximately 37.6% of the Australian market represented by the five major banks and BHP and Rio Tinto.

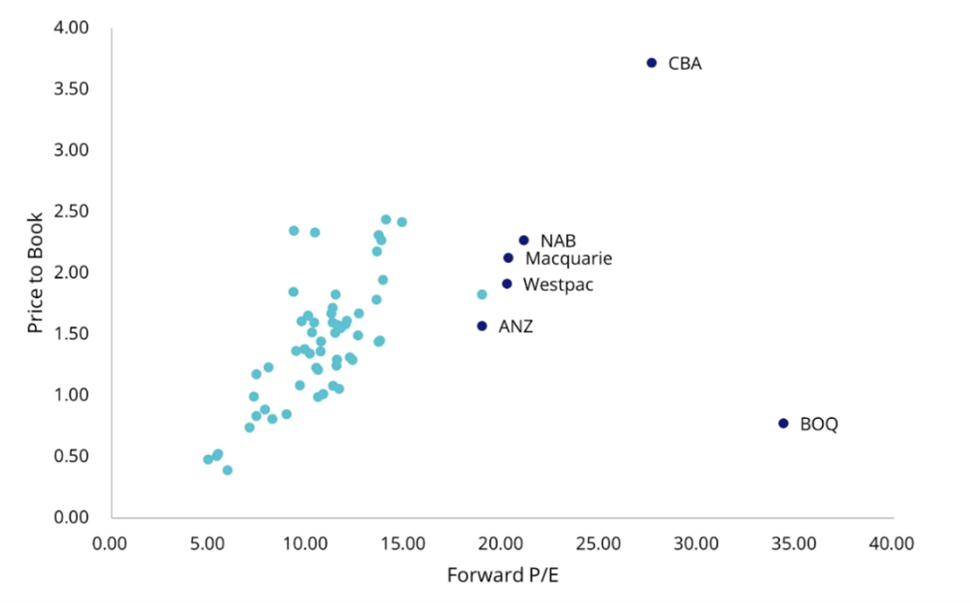

Valuations in some sectors, particularly the major banks, are now approaching historically high levels relative to both earnings and book value.

How to navigate current markets

It is likely that Australia will not feel the full economic impact of this conflict until the second half of the year.

Sustained higher fuel costs, combined with reduced fertiliser availability, are expected to pressure food production and contribute to further increases in food prices. At the same time, economists are forecasting additional interest rate rises, placing further strain on already indebted households.

An underappreciated risk is the growing pressure from union-led wage demands that many businesses may struggle to absorb. Combined with the accelerating adoption of AI, this raises the risk of a private sector pullback in hiring as firms focus on cost control and automation.

To date, employment has remained resilient, supported in part by continued expansion in the public sector. However, with government finances increasingly constrained by rising debt at both State and Federal levels, this support may not be sustainable.

This difficult economic backdrop is occurring alongside highly concentrated equity markets in both Australia and the US, where the largest companies are trading at elevated valuation multiples.

History rarely repeats, but it often rhymes. Now is a time to remain cautious.

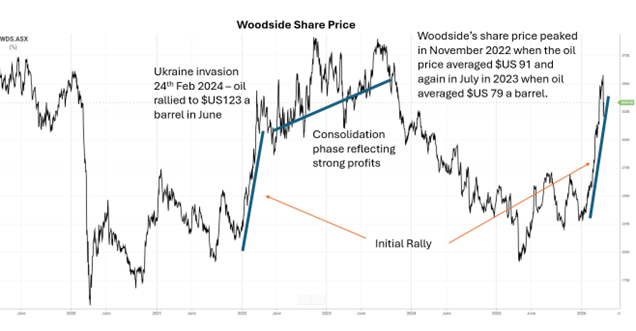

Last month, we discussed taking profits in Woodside and Santos. It now appears these companies may benefit from at least two years of elevated earnings driven by higher oil and gas prices.

Historical experience supports this view. During the Ukraine conflict in 2022, oil prices spiked sharply, and while they later eased, companies such as Woodside continued to perform strongly for an extended period due to sustained earnings strength.

In the current environment, Woodside and Santos continue to provide a useful hedge against further Middle East instability.

The current situation reinforces that oil and gas remain critical to the global economy. Australia, with its reliance on mining and transport, is particularly dependent on diesel.

We expect a renewed global focus on diversifying energy supply and increasing self-reliance. Companies such as engineering firm Worley, with strong exposure to the energy sector, are well positioned to benefit from increased investment in infrastructure and supply diversification.

We recommend maintaining a prudent cash allocation and selectively investing in high-quality industrial companies that have been materially sold down. Where appropriate, this may be funded by reducing exposure to sectors trading at elevated valuations, such as the Australian banks.

Please contact our office if you would like to discuss your portfolio in more detail.