Last night, Jim Chalmers announced the Federal Budget, which included significant proposed changes to the Australian taxation system. These changes appear intended to address the perceived inequality gap between younger and older Australians.

In summary, the four key changes most likely to impact you are:

- From 1 July 2027, capital gains tax calculations will change including the replacement of the 50% CGT discount with inflation-adjusted indexation and a minimum 30% tax rate on realised capital gains.

- From 1 July 2027, established properties purchased after Budget night will no longer be able to be negatively geared to generate a tax deduction.

- From 1 July 2028, a minimum tax rate of 30% will apply to all family trust distributions.

- From 1 April 2027, the removal of the age-based uplift of the private health insurance rebate.

We attach a summary of the proposed changes prepared by Colonial First State. Given the significance of these announcements, we encourage you to review this summary.

We have several initial thoughts on the Budget announcement, including the following.

At a Macro (National) Level

The Budget unveiled $77 billion in net tax increases over the 10-year forward estimate period. Despite this, underlying Budget deficits are forecast to total $150.5 billion over the next five years to 2030. This increases to $264.5 billion when funds directed into off-Budget vehicles for fuel security, renewable energy rollout and manufacturing subsidies are also considered.

The forecasts also assume substantial reform of the NDIS, with projected savings of $37.8 billion over the next 4 years that grows to $184.9 billion over the 10-year estimate period. This appears challenging given the current state of the NDIS. Likewise, the forecasts do not appear to account for the possibility of subsequent adverse economic conditions, including higher-than-expected inflation arising from the ongoing Middle East conflict, along with any subsequent economic shocks.

Consequently, despite the significant long-term increase in taxation projected in this budget, gross debt is forecast to increase to $1 trillion next year, with net debt forecast to climb to $616 billion.

Forecasts appear to present as an ‘optimistic’ base case, with the long-term risk that deficits and overall debt could increase materially from what is presently projected over the forward estimates’ period.

With the running of substantial deficits, the Budget is expansionary in nature and will likely place further pressure on the Reserve Bank of Australia to increase interest rates. The public sector appears set to continue to grow as an overall percentage of the Australian economy and at the expense of the private sector, with productivity likely to continue to suffer and consequently Australian living standards to remain under pressure.

In the Treasurer’s budget night speech, he highlighted that a key budget outcome was an expected additional 75,000 young homeowners over the next 10 years. This equates to 7,500 people per annum, which, across a population of around 25 million, is completely insignificant.

With some of the measures representing broken election promises, Labor is showing a willingness to expend political capital, and we suspect they may ultimately expend more than they initially expected. The proposed changes to family trusts, which Labor has positioned as tax structures that favour the rich, appear to lay the groundwork for the next Federal Election battleground, with these changes scheduled for implementation after the next election.

The breadth of the announced changes will substantially increase the complexity of Australia’s taxation system, which is likely to increase the cost of navigating it.

Potential outcomes from specific policy changes

1) Abolishing negative gearing on established dwellings

Passive property investment will lose appeal due to increased ongoing holding costs for investors. With tax benefits now favouring new dwellings, property investment may become more specialised and less accessible for many investors.

Existing negatively geared investors may become reluctant to sell, as the ability to negatively gear a future established property investment will be lost.

Property investors may also consider consolidating their property investments into their principal residence, which continues to retain its capital gains tax exemption.

2) Changes to the taxation of capital gains

Up to 30 June 2027, the 50% CGT discount will continue to apply, with indexation applying thereafter. As such, it may be appropriate to consider valuing assets as at 30 June 2027. This is likely to keep property valuers very busy.

With a base capital gains tax rate of 30%, although not applicable to Centrelink income recipients such as Age Pensioners, the benefit of timing a capital gain in a low-income year will reduce substantially.

Holding assets in a company structure may become relatively more beneficial, with gains converted to income and, if paid as fully franked dividends, potentially providing the opportunity to receive franking credit refunds.

3) Changes to the taxation of family trusts

For many, it may be possible to navigate around this tax through the payment of wages directly from a family trust, or through distributions to a corporate beneficiary that can subsequently pay a salary or fully franked dividend.

Who are the winners from the changes announced in the Federal Budget?

With many adverse taxation measures announced in the Budget, areas that have been excluded have, by default, become clear winners. The most significant of these is superannuation, which continues to retain all existing substantial taxation benefits.

Likewise, there are no changes to the taxation of estates or testamentary trusts. Consequently, estate planning is likely to become even more important going forward.

Finally, there are no changes to company structures or franking credits, including the refunding of franking credits. Labor may still be mindful of its 2019 election loss, where it proposed to abolish franking credit refunds.

As more Budget information comes to hand, we will discuss with clients individually on how best to navigate these changes in light of personal circumstances.

Operational update: Bank of Queensland (BOQ) to Macquarie transition

Changing topic to an operational matter, Horizon is in the process of moving all client portfolio bank accounts from BOQ to Macquarie Group. To this end, please expect notification from Macquarie in due course with the changeover date scheduled for the end of the financial year.

BOQ has advised that it is unable to meet the regulatory requirements for advisor linked bank accounts and will be closing them in November this year. Disappointingly, BOQ has also reneged on the interest rate it previously advised it would pay on these accounts, being the RBA cash rate less 0.10%, and is currently paying just 3.10%.

Going forward, Macquarie will offer two alternatives:

1. A base cash management account (CMA) account, paying 2.75%.

2. A linked Accelerator Account, paying 4.40%.

Both accounts are at call.

Importantly, Macquarie’s systems have been enhanced in recent years to make them compatible with investment advisers. A key security change that will occur as part of the move to Macquarie is that clients will need to use the Macquarie Authenticator App to approve one-off ad hoc transfers.

We will provide further guidance on how to install and use the Macquarie Authenticator App in due course.

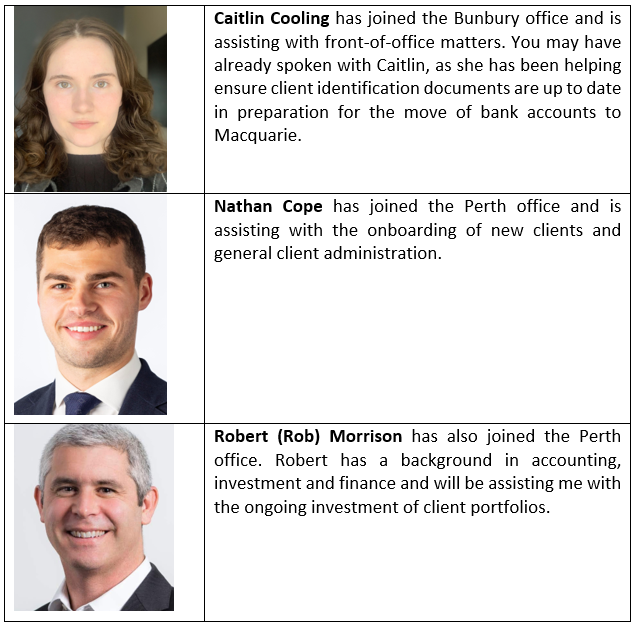

Horizon team update

I would also like to take this opportunity to introduce some new faces to the Horizon team.

The significance of the Federal Budget has made it the priority for this month’s letter. However, this is not to downplay the heightened investment risks we see emerging as the Middle East conflict continues.

We are continuing to build a defensive position for client portfolios, focusing on value-oriented companies, maintaining a high level of diversification and holding appropriate cash balances.

Next month, we look forward to providing further suggestions on alternative defensive income orientated investments to help provide both portfolio stability and income during what could become an increasingly turbulent period for investment markets.